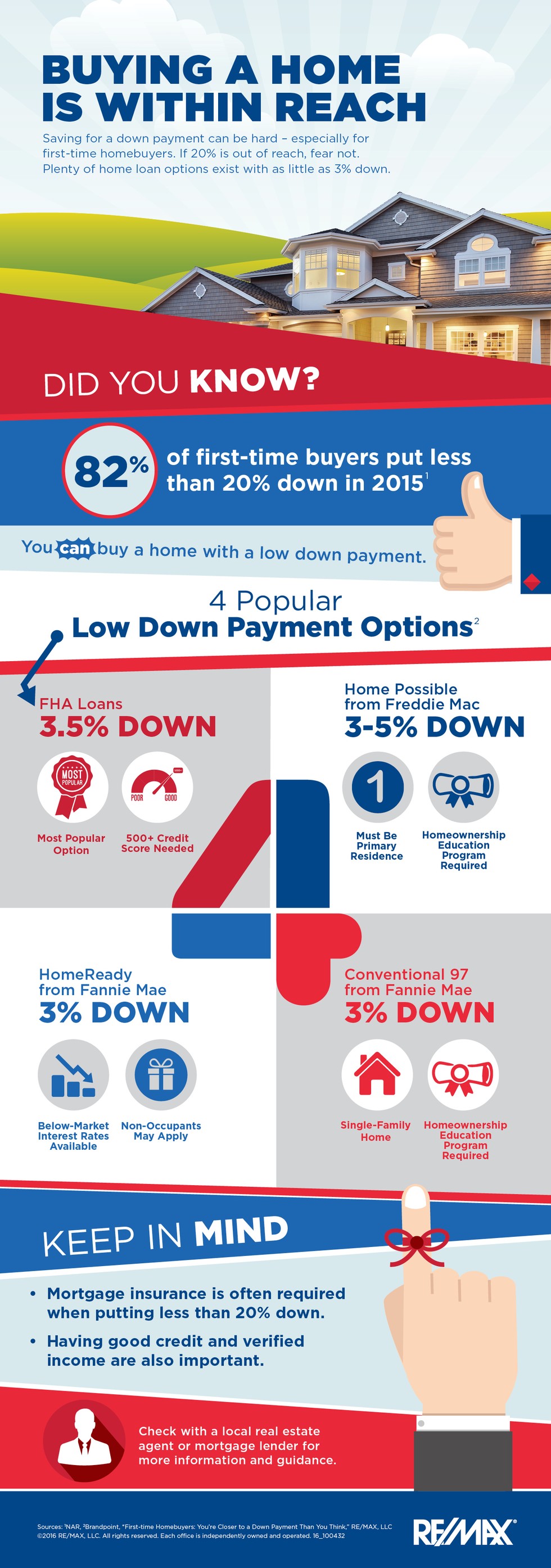

* FHA Loans — The mortgage of choice for first-time buyers. The most popular FHA loan option is the 203(b). The Federal Housing Administration (FHA) offers government-insured loans with as little as 3.5% down. You may qualify with a credit score of just 500, although there may be limitations on some condo purchases.

* Conventional 97 from Fannie Mae — Just 3% down will qualify you for a Conventional 97. You must apply for a fixed-rate mortgage on a single-family home that’s less than $417,000. You’ll also need to participate in a homeownership education program, and at least one of the purchasers applying for the loan must be a first-time buyer.

* Home Possible from Freddie Mac — This program allows you to put between 3% and 5% down – as long as you intend to 1) use the purchased house as your primary residence and 2) don’t currently own or share ownership of another house. You’ll also need to complete a required homeownership education program online.

* HomeReady from Fannie Mae — Another option that requires as little as 3% down, HomeReady can offer below-market interest rates. This program also allows non-occupant borrowers to apply; for example, parents can secure this type of loan for a young adult, who’s just starting to establish credit.

In addition to these mortgage options, there are also a variety of down payment assistance programs that may be available through your state or lender. Today, many loan programs allow for down-payment funds to come from third party sources, like cash gifts from relatives.

In addition to these mortgage options, there are also a variety of down payment assistance programs that may be available through your state or lender. Today, many loan programs allow for down-payment funds to come from third party sources, like cash gifts from relatives.

Something to keep in mind – putting less than 20% down can also result in the additional monthly cost of Private Mortgage Insurance (PMI). However, if your home value is appreciating, PMI can be eliminated in a few years through refinancing.